New Territory Search & Recommendation (District Manager)

A data‑led territory search helps banks optimize branch networks by combining internal performance data with external indicators such as demographics, income, consumption, signals like local activity and live feeds for the selected region. The view enables faster, more confident decisions on where to expand, rebalance, or optimize operations - helping banks managed customer alignment and branch profitability.

Multi-year Project & Planning (District Manager)

Once a location is shortlisted, multi-year forecasting enables branch managers to build a rigorous 5-year business case by projecting customers, revenues, and costs using local market and economic indicators. This creates a clear, data-backed view of viability and risk—allowing leadership to approve, fund, and execute new branches with confidence and defined timelines.

Agent Supervisor Overview & Management (Branch Manager)

A centralized agents overview enables banks to manage large field networks with clarity and control by tracking onboarding status, location, activity, limits, and performance in near real time. This allows branch and regional teams to quickly identify gaps, optimize coverage, manage risk, and ensure agents are productive, compliant, and aligned with local demand.

Territory Overview (Agent Supervisor)

A territory‑level overview gives supervisors clear visibility into the agents they manage, including coverage areas, activity levels, cash positions, and service performance. This enables day‑to‑day coordination, quicker issue resolution, and better workload balancing. And also ensures field operations are run smoothly while staying aligned with branch targets and compliance requirements.

Pan-country banking penetration

A time‑planning tool helps on‑field agents organize daily customer visits by optimizing routes, schedules, and service priorities based on location and workload. This is designed to improve productivity, reduces travel inefficiencies, and ensures customers are served on timewhile. The visibility also reflect in the supervisor and branch manager's dashboards, keeping them abreast with status and operational gaps.

Customer Form Capture (On-field Agent)

A tablet‑based customer form enables agents to guide customers through data capture during field visits, helping clarify banking terms and processes while addressing digital and literacy gaps. This assisted, standardized interaction improves customer understanding and trust, enhances data accuracy, and ensures secure, seamless flow into banking and compliance systems.

Pan-country banking penetration

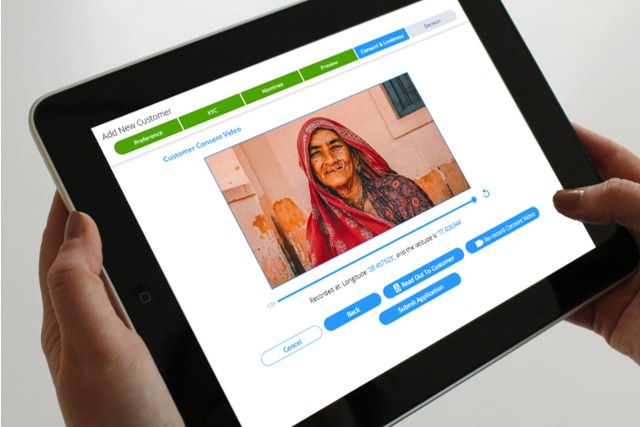

At the end of the onboarding flow, live customer capture and video‑based KYC enable real‑time identity verification, with the system guiding the customer through spoken prompts and confirmations. This assisted interaction improves transparency and understanding, builds trust, and ensures regulatory compliance especially for customers unfamiliar with digital banking processe or document related challenges.

Desktop App (Banker & Agent Supervisor)

Desktop App (Banker & Agent Supervisor) Table App (On-field Agent)

Table App (On-field Agent)